Objectives and Key Results (OKRs) and Balanced Scorecards (BSC) are performance management frameworks for defining and tracking goals. BSC arrived on the strategic management structure scene in the early 90s, a couple of decades after Andy Grove co-founded Intel and launched the modern OKR system. John Doerr, Grove’s mentee, would later adopt, spread, and popularize the OKR system throughout Silicon Valley and beyond with Measure What Matters.

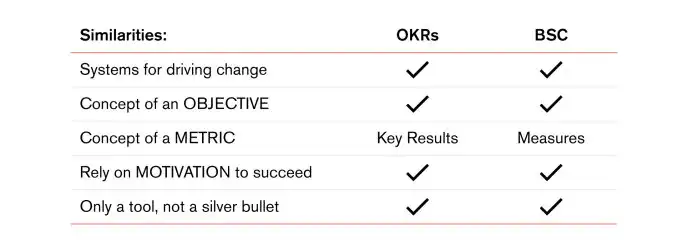

Both OKRs and BSC are systems for driving change. They both seek to transparently communicate what a team or organization is trying to achieve, align that departmental work with strategy, and measure all strategic progress towards pre-determined, desired outcomes.

To do this, they both rely on motivation as a means for the organization to succeed.

But while there are a lot of similarities between OKRs and BSC in intent, there are big differences in their approaches to strategy and their overall techniques in achieving the objective.

In this resource, we’ll explain what those differences are as we answer these questions:

- What’s the main difference between OKRs and BCS?

- How often is BSC set?

- How often are BSC reviewed?

- Are compensation and bonuses tied into BSC?

- What is an example of a BSC and a strategy map?

- Can BSC and OKRs be used together?

- Where is BSC practiced?

- If I have more questions, where should I send them?

What’s the main difference between OKRs and BSC?

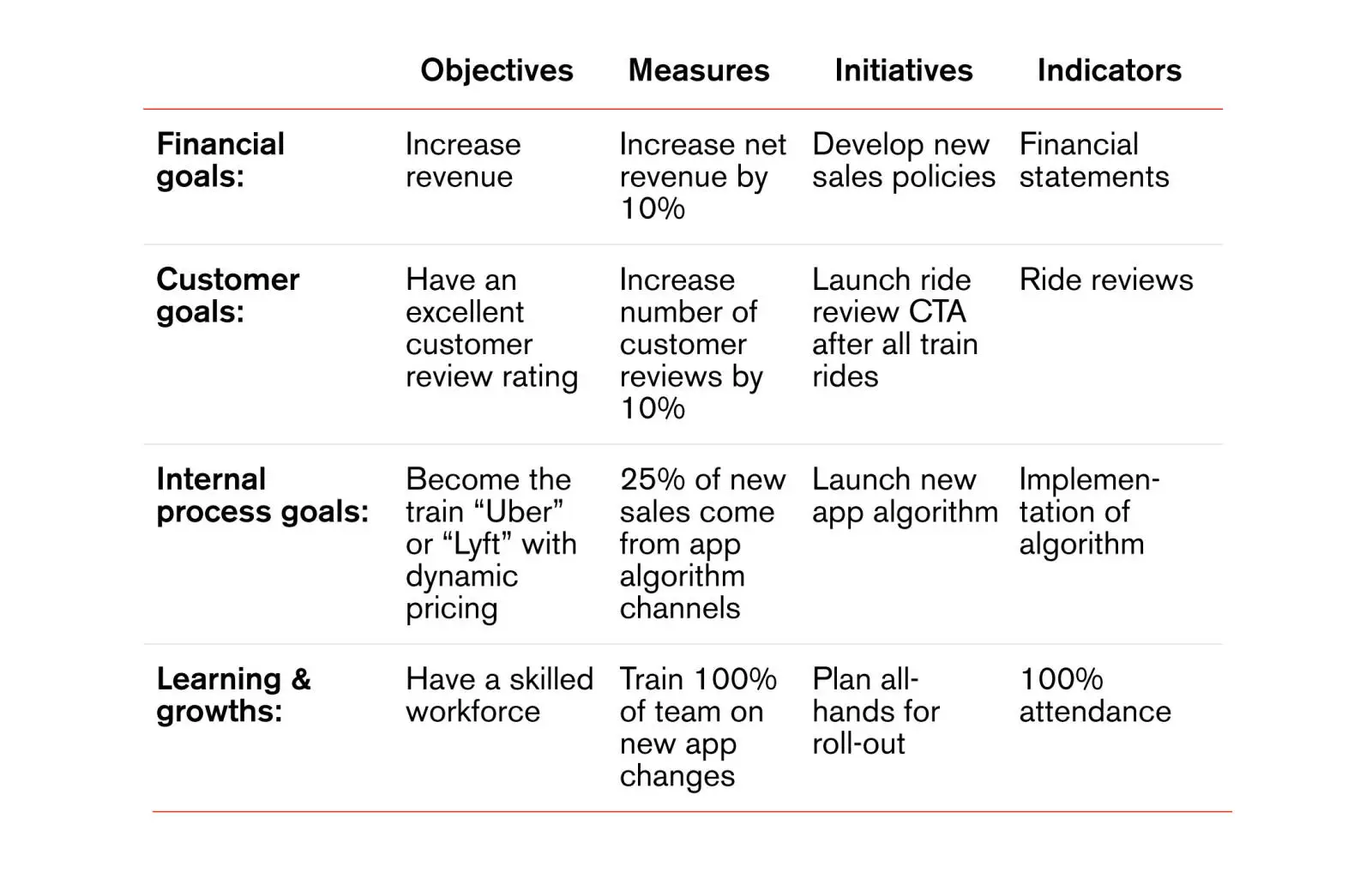

The first main difference between OKRs and BSC is that BSC relies on a holistic strategy map with “parameters for creation," meaning there is a set structure for how Objectives are supposed to be crafted in four separate but related aspects of performance: Financial, Customer, Internal Processes, and Learning and Growth.

With BSC, the financial aspect is the most important and is used to craft measurement parameters to answer these questions, as provided by ClearPoint Strategy:

- Financial goals: “What financial goals do we have that will impact our organization?"

- Customer goals: “What things are important to our customers, which will, in turn, impact our financial standing?”

- Internal Process goals: “What do we need to do well internally, in order to meet our customer goals, that will impact our financial standing?"

- Learning and growths: “What skills, culture, and capabilities do we need to have in our organization in order to execute on the process that would make our customers happy and ultimately impact our financial standing?”

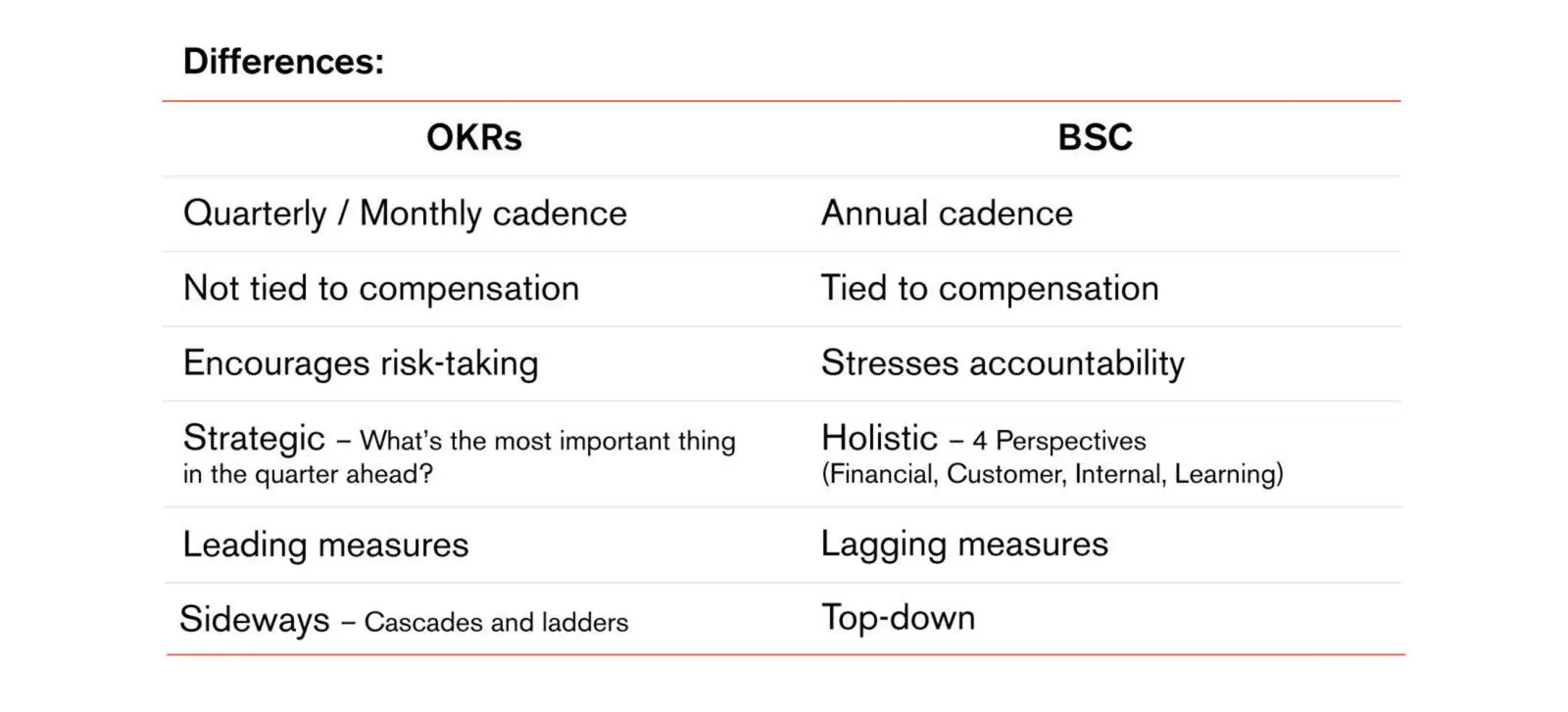

Once one of the four performance aspects is decided is when important goals can be crafted to fit that aspect framework. A BSC framework includes Objectives, Measures, Initiatives, and Indicators. Within this framework, BSC is top-down and emphasizes lagging measures—output-oriented goals like the aforementioned financial benchmarks.

OKRs, on the other hand, not only cascade but also ladder. Because of this, they also focus on leading measures, or inputs, such as expanding a product offering to the Asia-Pacific region by the end of the quarter.

Both BSC and OKRs have the same definition for Objectives which is, bottom line, what is to be achieved. However, with Balanced Scorecard, there can be a lot more Objectives than the OKR system would ideally allow.

At What Matters, we recommend a maximum of 2-3 Objectives at any given time, whereas BSC can have 10-15 Objectives.

In BSC, “Measures” are the same as “Key Results.” But BSC recommends only having 1-2 measures per Objective, while with OKRs you can have 3-5 Key Results.

In BSC, Initiatives (sometimes also called “Projects,” “Actions,” or “activities outside of the Balanced Scorecard”) are developments needed to complete an Objective. Most companies have a couple of initiatives for every Objective. An example would be to complete a new app rollout of employee surveys for team satisfaction for a Learning and Growth Objective.

All in all, OKRs do not use parameters for creation. In OKRs, the team gets to decide what the priority is. This means that risk taking is encouraged, whereas, because of the emphasis on outputs like financial goals, BSC stresses accountability to a pre-planned set of activities.

For a better visualization, take a look at these two charts:

BSC and OKR Examples

For an example in the differences of Balanced Scorecard vs. OKRs, consider this BSC example of a commuter rail system:

With BSC, any cell item could be broken down further to truly explain what the measurements of success would be for that item. For example:

As you can see, OKRs help to define what a successful launch of a ride review program would look like with hard numbers and an input. This micro-defining of success that differentiates BSC and OKRs may be due to the different cadences of the two strategies.

How often is BSC set?

BSC is typically drafted and designed to stay in place for a minimum of one year. And because of the cycle, performance tends to be annual and tied to financial goals.

OKRs, alternatively, are designed to stay with an organization for one cycle, typically a quarter but sometimes a month. After that, OKRs are graded, and new OKRs are drafted. But throughout the cycle, OKRs are designed to be frequently reviewed so adjustments can be made as the team learns more about how to achieve an ambitious goal.

How often are BSC reviewed?

Traditionally, BSC is reviewed annually, with no mandated check-ins to see if a strategy is working.

This is the opposite of OKRs, the success of which is inextricably linked to another acronym, CFRs. CFRs is the second part of the OKR goal-setting framework and stands for Conversations, Feedback, and Recognition. CFRs allow the often black-or-whiteness of OKRs the necessary context and conversation to talk about if a goal is still relevant — and this does not mean just once when OKRS are graded at the end of an OKR cycle.

CFRs should be happening throughout the OKR cycle and should take place in, ideally, weekly 1:1s.

Reviewing OKRs makes sure they are still relevant and accurate as new information is learned throughout a cycle. It also allows time for conversations to happen that can help push critical capabilities to the forefront, remove blockers, and raise shifting priorities.

This continuous performance management is one big difference between OKRs/CFRs and BSC.

Are compensation and bonuses tied together in BSC?

BSC also differs from OKRs in that it directly correlates financial goals with performance reviews, bonuses, and compensation. The intention is to encourage goal-setting clarity and transparency for the desired targets.

OKRs, however, are not intended to be tied to performance. They should be divorced from the goal-setting process so teams are motivated to shoot for targets they might otherwise miss without feeling the risk of being penalized financially.

As Laszlo Bock, Senior Vice President of People Operations at Google from 2006 to 2016, states, “You can absolutely pay a sales organization on sales quotas. You want their sales numbers to be part of their OKRs. But just remember, anytime there’s a sales incentive plan it creates perverse incentives, whether it’s tied to OKRs or not.”

Outcomes of these perverse incentives when the goal is pure revenue without a balancing “quality Objective” could be things like volume pushing without profits or prioritizing enterprise contracts that may look like a lot of immediate dollars but wither in the long run.

Keep in mind, both systems are tools, rather than silver bullets. Neither one takes the place of a healthy culture or great leadership, but they can each put guidelines in place to help teams steer to collective success.

Can BSC and OKRs be used together?

Yes, BSC can be used with OKRs in a complementary way, particularly at the senior level. There, the BSC strategy map can help executives and other leadership craft OKRs by seeing what’s important for that year and then breaking it down — then up.

For example, a strategy map provides a great visual of how OKRs may cascade down through an organization. And since healthy organizations strive to have half of their goals come from the bottom-up, a BSC strategy map is a great way to make sure that company seniors have checked-in on everyone on the frontlines.

From there, OKRs function to help an org keep a pulse on what is the most important thing to individual departments and teams for the next month or quarter with Key Results and CFRs. So while BSC helps develop holistic approaches to strategy, OKRs help make sure strategies don’t become too macro, have more defined and time-sensitive measurements, and are not all output goals.

Where is BSC practiced?

BSC remains very popular and is practiced by many popular companies to this day. Volkswagen, Wells Fargo, Apple, and Verizon are some household names that use BSC.

If have more questions, where should I send them?

Have you tried OKRs and BSC? Share your experience with us, and be sure to check out our OKR Examples and case studies.

Or, if you’re looking for an OKR coach, check this out.

If you’re interested in starting our OKRs 101 course, click here.